In a speech on the Senate floor, Finance Committee Chairman Orrin Hatch (R-Utah) reiterated the momentum behind reforming our nation’s tax code and said lowering the U.S. corporate tax rate from one of the highest in the world to one of the lowest is a top priority in current tax reform efforts.

“Our high corporate tax rate isn’t just a burden on faceless corporations or rich shareholders. The burden is disproportionately borne by the factory workers, the scientists, and even the janitors who work for corporations, large and small,” Hatch said. “A reduced corporate tax rate would allow American companies to compete with their international counterparts on a more level playing field. A reduced corporate tax rate would mean that fewer businesses would move offshore, taking their jobs and investments elsewhere. A reduced corporate tax rate would incentivize more new companies to set up shop in the U.S., and lead more established companies to invest their capital and hire workers here, rather than in lower tax jurisdictions found in places like Canada, the U.K., Ireland, or elsewhere.”

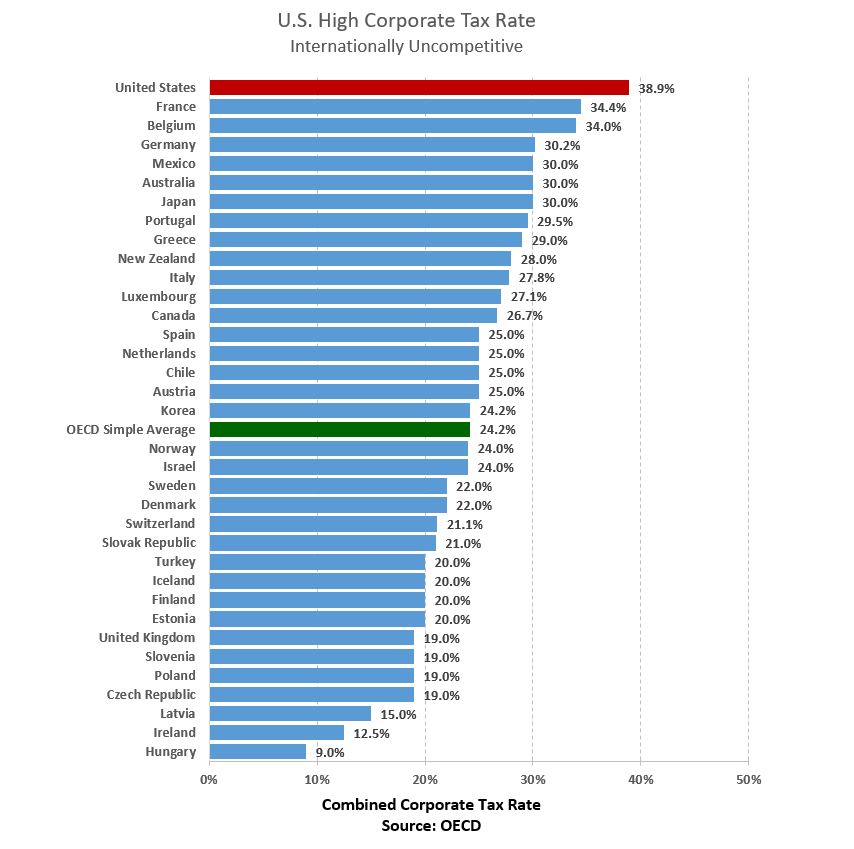

Background: The United States has the highest statutory corporate tax rate in the developed world. America’s effective corporate tax rate – the actual rate paid after deductions and credits – is also globally uncompetitive, ranking fourth among G-20 countries.

The complete speech as prepared for delivery is below:

Mr. President, I rise today to once again discuss the ongoing effort to reform our nation’s tax code.

Over the past several years, I’ve come to the floor often to make the case for tax reform by highlighting the many shortcomings of our current tax system and discussing the benefits we could reap by making the necessary changes.

Over the last six years while I have served as the lead Republican on the Senate’s tax-writing committee – both as Ranking Member and as Chairman – I have made tax reform my top priority. And, right now, I believe there is more momentum in favor of tax reform than we’ve seen in decades.

To capitalize on that momentum, reform advocates, like myself, need to continue to make the case for updating and fixing our broken tax system. Toward that end, I intend to come to the floor often in the coming weeks and months to discuss various aspects of our tax system and make the case for reform.

In my view, we need to go back to the drawing board and fundamentally rethink our entire tax system. This includes both the individual, as well as business side of the tax ledger.

Today, I want to talk specifically about our nation’s business tax system, with a particular focus on the corporate tax.

Let’s get the obvious out of the way first: The United States has the highest statutory corporate tax rate in the industrialized world. Looking at effective corporate tax rates tells an equally gloomy story of a lack of American competitiveness. I’ll have more to say on that in a minute.

I know some like to rail on corporate America and claim that they aren’t paying their fair share, but the facts tell a different story. Companies doing business in the U.S. are saddled with statutory tax rates that are higher than any other industrialized country.

This isn’t just a Republican talking point. Members and commentators from both parties and across the ideological spectrum have acknowledged that this is a problem.

For example, just last year, former President Bill Clinton argued for a reduction in corporate tax rates, noting that he had urged for the corporate tax to be raised to 35 percent when he was president because “it was precisely in the middle of OECD countries. It isn’t anymore.”

Early in his presidency, President Obama said: “Our current corporate tax system is outdated, unfair, and inefficient.” He also said that our corporate tax system “hits companies that choose to stay in America with one of the highest tax rates in the world.”

In addition, my counterpart on the Senate Finance Committee, Senator Wyden, has introduced legislation that would reduce corporate tax rates by more than 10 percent.

And, in a Finance Committee report in 2015 on international tax reform, put out by a working group co-chaired by my friends and colleagues Senators Portman and Schumer, it was clearly stated that: “No matter what jurisdiction a U.S. multinational company is competing in, it is at a competitive disadvantage.”

And there are plenty of other examples of prominent Democrats who have recognized the impact of our obnoxiously high corporate tax rate.

I want to turn back to President Clinton’s point though, Mr. President, because it is an important one.

We must always remember that businesses are, by and large, rational actors, making decisions based on what will help grow their business and what will cause it to stagnate or move backwards. Such decisions inevitably include where a company will do business and where it will be incorporated.

According to the Organisation for Economic Cooperation and Development, or OECD, businesses contemplating investment and incorporation in the United States must first come to terms with the largest combined corporate tax rate among OECD member countries, which is currently at 39.1 percent.

Now, some of my friends on the other side of the aisle like to counter these inconvenient facts by acknowledging the difference between effective tax rates, which are rates after accounting for deductions and credits, and statutory tax rates.

Of course, even when taking those differences into account and focusing solely on effective rates, the United States only falls from highest to the fourth highest corporate rate among countries in the G20 – and that is according to 2012 data that doesn’t yet capture recent tax reforms in the U.K. and elsewhere. In other words, whether we’re talking about effective rates or statutory rates, in the U.S., we’re talking about some of the highest corporate tax rates in the world. And as the working group co-chaired by Senators Portman and Schumer made clear, this translates into American companies constantly being put at a competitive disadvantage.

It doesn’t take a PhD in economics to recognize that this has had a negative impact on our economy and the ability of American job creators to compete on the world stage.

As a result of the astronomically high corporate tax rates in our country, we’ve seen companies – that, keep in mind, have duties to their shareholders – engage in inversions, earning-stripping, and profit shifting, all of which erode our tax base and drive away American ingenuity and innovation. These types of activities ship jobs, economic activity, intellectual property, and capital offshore, rather than keeping it right here in America. The primary driver behind most of these practices – practices that have been decried in the harshest rhetoric by some of our friends here in the Senate – is the desire to avoid – or at the very least mitigate – the impact of the U.S. corporate tax.

While I’m no fan of inversions or foreign takeovers or aggressive tax planning techniques that shift profits around the globe in search of low taxes, and I don’t want to see any unnecessary erosion of the U.S. tax base, I can hardly fault any company for simply responding to the incentives created by our business tax system and the competitive actions of other countries who’ve been lowering their corporate tax rates.

Unfortunately, instead of recognizing the perverse incentives of our current tax system, coupled with companies’ duties to their shareholders, many of my Democrat friends – most notably some prominent officials in the previous administration – have derided the executives and board members making these decisions, claiming that they lack, in the words of our previous U.S. Treasury Secretary, “economic patriotism.”

The truth is, when it comes to our business tax system, some of our friends have buried their heads in the sand. Let’s take a quick stroll through recent history.

In the 20 years between 1983 and 2003 there were just 29 corporate inversions in the United States.

In the 11 years between 2003 and 2014 – a period spanning both Democrat and Republican presidencies – there were 47 – nearly double the number in half the amount of time.

A quick review of changes in other industrialized nations’ tax schemes will show that, while the United States has stubbornly maintained the same corporate tax rate for more than three decades, other countries have nimbly adapted to the growing competition in the global marketplace.

Now, Mr. President, I’ve spoken at length about inversions before, so I will not belabor that issue now. What I do want to say is that when I talk to board members and CEOs of some of the largest companies in our country, they tend to be unequivocal when asked why they feel pressure to invert. Almost uniformly, their answer is our outrageously high corporate tax rate.

Personally, I think this is one of the reasons why my friends and colleagues who sit on committees that regularly engage in these topics have come to recognize the level of our corporate tax rate as the major problem it is.

And, when I talk to constituents in Utah, and Americans across the country, I hear of stagnant growth in wages and income, concerns over lack of opportunities and jobs, and worries about whether their employers will continue to operate here in America.

Of course, the problem with our corporate tax system isn’t just that it incentivizes companies to move offshore or discourages businesses from forming here in the first place. The problems actually run much deeper.

Since 1947, the average growth of inflation-adjusted GDP in the U.S. has been 3.2 percent. Unfortunately, in the eight years of the Obama administration, the growth rate was an anemic 1.8 percent. Now, I know that several of my colleagues would, in response to those data points, argue that much of that is due to the great recession that took place at the initial stages of President Obama’s time in office.

However, a quick review of the quarterly growth rates since 1947 will show that there are normally periods of growth following recessions as the economy rebounds and the values of assets normalize. In the case of the great recession of 2008 to 2009, that normal rebound did not occur, and a big reason why is the downward pressure imposed by our outdated tax scheme. And, let’s remember, the recession ended in June 2009, more than eight years ago.

Now others still might argue that this is all academic.

They might even be brazen enough to claim that, when we talk about the corporate tax rate, we’re talking about the problems of the rich, and not the middle class.

Again, anyone making such an argument would simply be ignoring the facts.

Make no mistake, Mr. President, the crippling corporate tax rate in our country has stifled growth and investment in American businesses, and this doesn’t just impact Wall Street investors or rich CEOs – it has a negative effect on the middle class and on lower-income workers. That effect comes in the form of fewer jobs, less investment in America, and sluggish growth in productivity that fuels wage and income growth.

Since 1953, the United States’ real median family income – meaning that half of the country earned more, and half of the country earned less – has grown at an average rate of 1.3 percent.

Under the Obama administration that same indicator – one of the best indicators of the true status of the middle class – grew at approximately half that rate, or 0.7 percent.

The growth of the average hourly earnings of production and nonsupervisory works during the Obama administration was half of the historic long-run average.

What is more, labor force participation was set firmly on a downward trajectory throughout the Obama administration, and has yet to recover.

As you can see, Mr. President, there is clear evidence that the economy is not working well for many American workers and middle-class families. Anyone arguing that our current tax system is a benefit to the middle class is, in my view, misinformed or being deliberatively misleading.

Over the years, I’ve seen many of my friends on the other side come to the Senate floor demanding new standards, higher wages, and increased protections for middle-class workers. Yet, many of the tax policies they tend to support would have the opposite effect.

There is almost universal agreement among economists that the corporate tax is the most inefficient tax in existence. In addition, a large percentage – some economists say as much as 75 percent – of the burden imposed by the corporate tax is borne by a corporation’s employees.

In other words, Mr. President, our high corporate tax rate isn’t just a burden on faceless corporations or rich shareholders. The burden is disproportionately borne by the factory workers, the scientists, and even the janitors who work for corporations, large and small.

A reduced corporate tax rate would allow American companies to compete with their international counterparts on a more level playing field.

A reduced corporate tax rate would mean that fewer businesses would move offshore, taking their jobs and investments elsewhere.

A reduced corporate tax rate would incentivize more new companies to set up shop in the U.S., and lead more established companies to invest their capital and hire workers here, rather than in lower tax jurisdictions found in places like Canada, the U.K., Ireland, or elsewhere.

Mr. President, our shared goal should be to make the United States an inviting place to locate a business, invest, hire workers, and create new ideas and products, but that will not be the case so long as we cling to our punitive corporate tax system.

Now, of course, when it comes to tax reform, our focus needs to move beyond the corporate tax rates.

We need to talk about making the individual tax system simpler and fairer, and offer tax relief to the middle class and small, pass-through businesses.

We need to talk more about fixing our international system to further improve the competitiveness of American job creators and prevent further erosion of our tax base.

And, we need to remove burdens on savings and investment that keep middle class Americans from generating and accumulating wealth for the future.

I’m going to talk more about all of these topics – and others – in the comings weeks and months. All of the improvements that we can make on these tax issues will become key elements of an effective tax reform package. In addition, I believe they are all areas where Republicans and Democrats can find agreement, IF we are all committed to the same goal: Growing our economy to benefit the middle class.

As I’ve said here on the floor many times, tax reform does not have to be another partisan exercise. I hope my Democratic colleagues will opt to join Republicans in this effort. As they have acknowledged the problems with our current tax system, I sincerely hope they’ll want to work with us to find a way to fix it.

Like I said, Mr. President, I’ll have more to say in the near future. But these issues – our outdated business tax system and profanely high corporate tax rate – will not simply go away. I, personally, am committed to fixing these problems and will work with anyone who is willing to join the effort in good faith.

{kind=link}